The Inflation Story Investors May Be Missing

A unique second wave of inflation may already be emerging, driven less by strong demand and more by supply constraints, tariffs, and geopolitical pressures that could challenge markets still dependent on falling rates and easy liquidity.

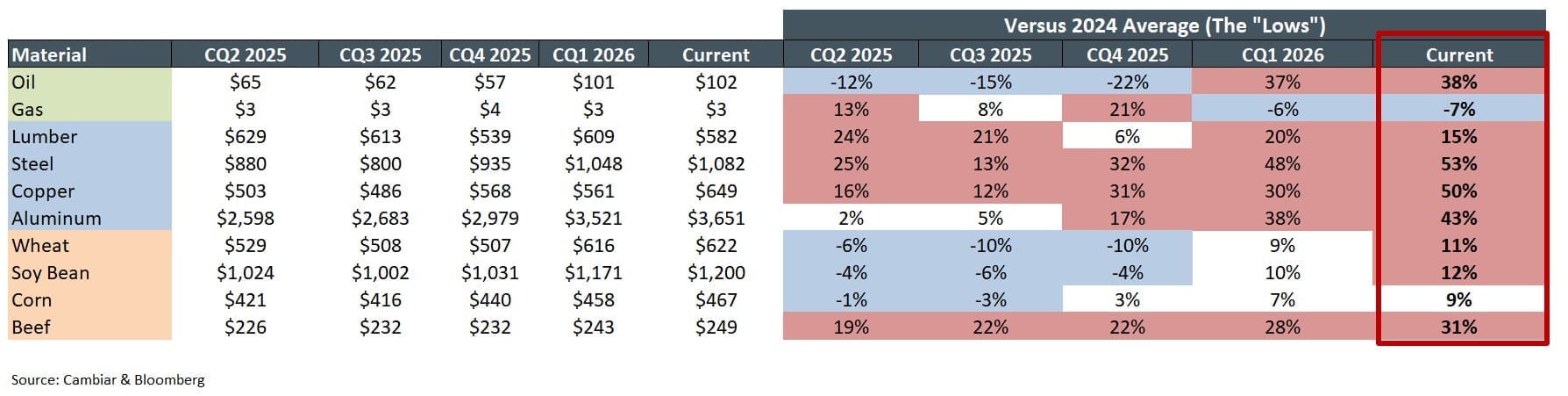

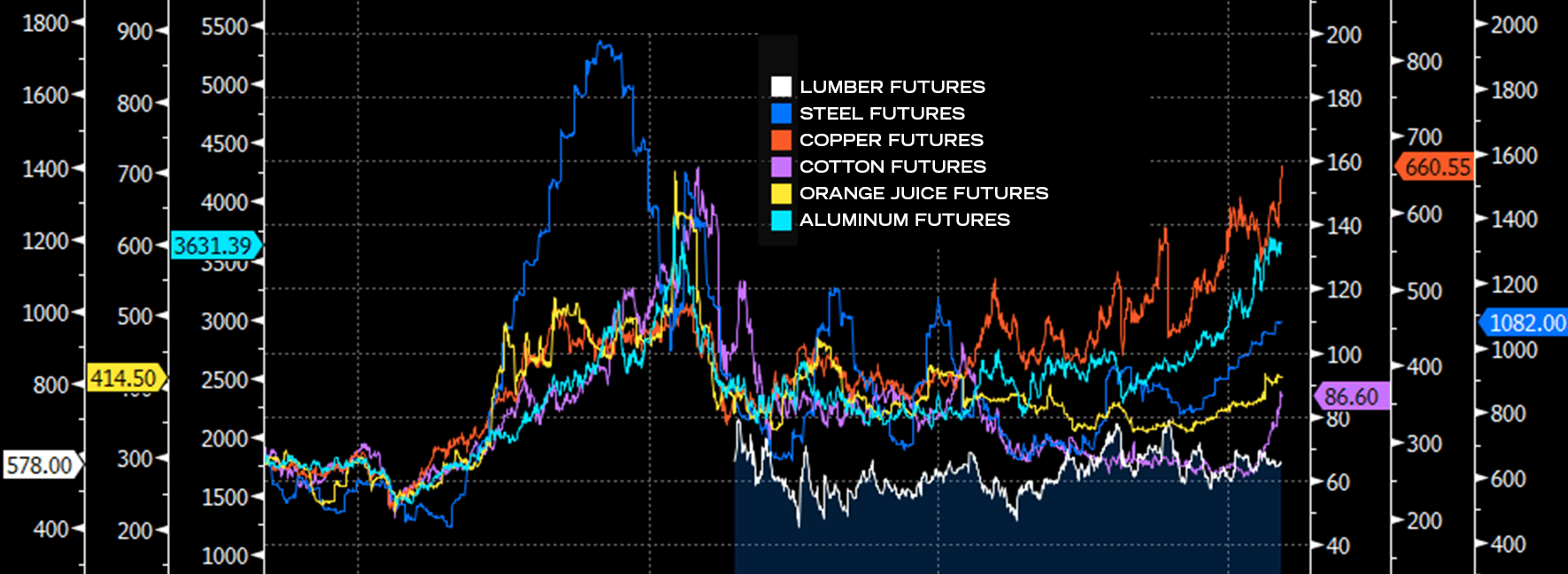

A unique second wave of inflation may already be underway. The charts below highlight meaningful price increases across several of the most economically important commodities tied to the U.S. industrial and consumer economy, including food, steel, aluminum, oil, and cotton.

Source Bloomberg

What makes this cycle different from the 2020-2021 inflation surge is that demand remains relatively weak across many areas of the economy. Historically, broad-based commodity inflation is often driven by strong economic growth and rising consumption. Today’s backdrop appears far more supply- and policy-driven, influenced by factors such as tariffs, geopolitical tensions, reshoring efforts, and years of underinvestment in commodity production capacity. There was substantial investment in production capacity in 2021-23, which drove weaker commodity prices in 2024-25.

Notably, several commodities such as steel, aluminum, and food products were already trending higher well before the recent escalation in the Middle East. Others, including oil and cotton, experienced sharp moves earlier this spring. The synchronized nature of these increases is important because these inputs ultimately flow through large portions of the economy.

While commodities themselves account for roughly 25% of headline CPI, their downstream impact is significantly larger through products and services embedded in core inflation. Inputs such as steel, cotton, fuel, and agricultural products influence everything from housing materials and transportation costs to apparel, industrial equipment, and consumer goods. As a result, sustained increases in these areas can exert renewed upward pressure on inflation, even in a slower-growth environment.

Industrial companies are already beginning to respond through price increases and pricing adjustments. In many cases, management teams remain far more willing to pass through higher input costs after navigating the inflationary environment of the past several years. While near-term margin pressure may emerge in certain industries, particularly those with weaker pricing power, the adjustment period could prove shorter-lived than many investors expect.

The broader market implication is significant. If inflation remains structurally higher despite moderating economic demand, it could create a far more challenging environment for markets that have become conditioned to falling rates and abundant liquidity. Sectors heavily dependent on cheap financing, including housing, autos, private equity, and highly levered areas of the economy, may face a more difficult road ahead even if economic growth slows.

More importantly, this type of environment tends to expose the difference between companies that simply benefited from easy money and those with genuine business strength. Businesses with pricing power, strong balance sheets, durable cash flows, and operational flexibility historically separate themselves when input costs rise, and capital becomes more selective.

We are already seeing early signs of this dynamic emerge. Airlines have begun adjusting fares to offset higher fuel costs. Industrial companies are passing through price increases tied to inflation in steel and aluminum. Consumer brands continue raising prices on apparel and packaged goods as cotton, freight, and agricultural costs move higher. Meanwhile, many lower-quality businesses with heavy debt burdens are finding it increasingly difficult to absorb higher financing and input costs simultaneously.

This backdrop may also challenge one of the market’s dominant assumptions over the last decade: that any economic slowdown will quickly lead to aggressive Fed easing and a broad rebound in all asset prices. If inflation proves more supply-driven and structurally persistent, policymakers may have less flexibility than investors expect.

For investors, the takeaway is clear. Markets may be entering a period where fundamentals matter more again. Balance sheet strength, pricing power, non-discretionary demand, valuation discipline, and active security selection could become increasingly important in separating long-term winners from businesses that were simply beneficiaries of an era defined by low rates and easy capital. Volume growth is close to zero for almost everything that’s not data centers/AI, so idiosyncratic, non-cyclical demand streams are vital right now.

Equally important, environments like this often create meaningful dispersion beneath the surface of the market. While passive strategies may remain heavily concentrated in areas benefiting from momentum and liquidity flows, active management can become increasingly valuable in identifying businesses with resilient demand profiles, attractive valuations, and the operational flexibility to navigate changing economic conditions. In our view, the next phase of the market may rely less on easy money and more on fundamental business strength, disciplined capital allocation, and selective risk-taking.

Certain information contained in this communication constitutes “forward-looking statements”, which are based on Cambiar’s beliefs, as well as certain assumptions concerning future events, using information currently available to Cambiar. Due to market risk and uncertainties, actual events, results or performance may differ materially from that reflected or contemplated in such forward-looking statements. The information provided is not intended to be, and should not be construed as, investment, legal or tax advice. Nothing contained herein should be construed as a recommendation or endorsement to buy or sell any security, investment or portfolio allocation.

Any characteristics included are for illustrative purposes and accordingly, no assumptions or comparisons should be made based upon these ratios. Statistics/charts and other information presented may be based upon third-party sources that are deemed reliable; however, Cambiar does not guarantee its accuracy or completeness. As with any investments, there are risks to be considered. Past performance is no indication of future results. All material is provided for informational purposes only and there is no guarantee that any opinions expressed herein will be valid beyond the date of this communication.