Tough Year for Globalists

U.S. markets continue to outperform their international counterparts in 2018, with the performance gap widest on record. Cambiar examines what could turn the tide.

Capital Concentration Into Dollar Assets Means 2018 is a Tough Year for Globalists

We are providing an update to current global equity market conditions as of mid-September, and why we believe they are unfolding in the manner that they are. The goal is to help investors make thoughtful decisions as current processes continue to develop.

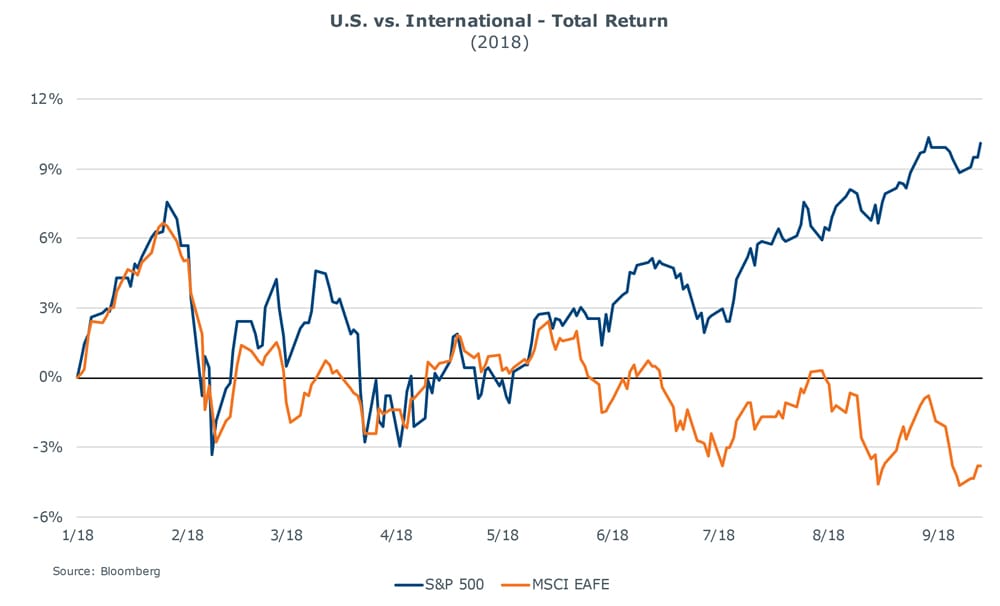

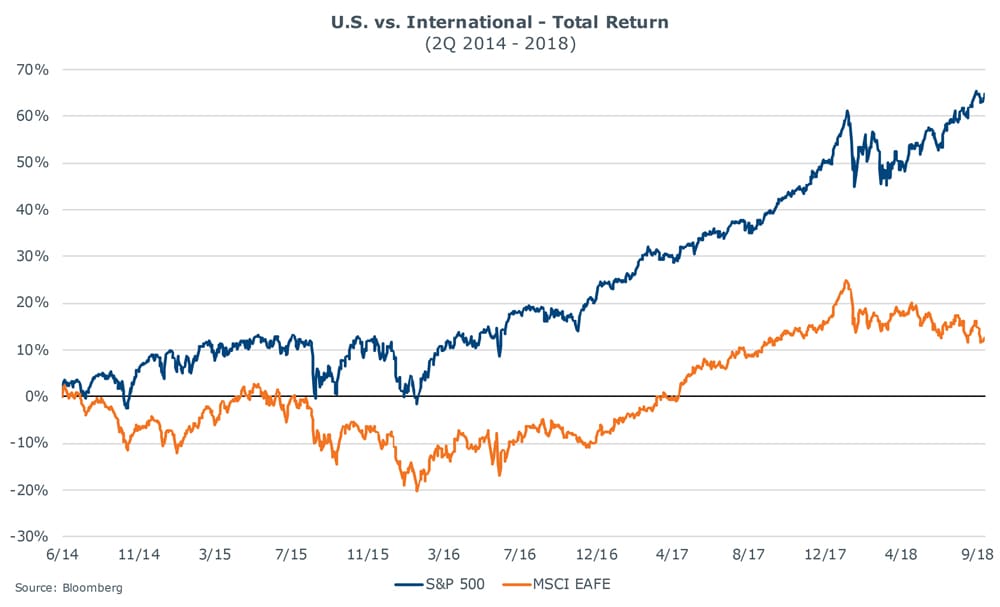

Extending back to mid-2014, U.S. stocks have roundly trounced international alternatives. The S&P 500 Index has returned 60% (cumulative), vs. 10% for the MSCI EAFE Index. The discrepancy has become particularly extreme in 2018, with U.S. stocks posting a 9% gain through August, vs. -4% for the EAFE. Bull markets and bear markets have generally been positively correlated within global equities – but not this one. The performance gap over the last several years represents the widest on record. It has not paid to be a globalist in 2018, nor to any great extent in the current decade, for that matter.

We believe there are three major factors leading to this discrepancy:

- Better U.S. corporate earnings growth,

- An out of sync global interest rate regime leading to capital concentration in U.S. dollar assets (such as stocks), and

- Financial pressure on Emerging Markets as a consequence of capital concentration into the dollar/capital flight from EMs.

Realistically, we don’t see these primary factors shifting decisively in a different direction between now and year-end. However, we believe there is a reasonable case to be made that this narrative shifts in 2019+.

There have been various forms of capital concentration in the post-GFC time period. Examples include a preference for Emerging Market stocks during the early recovery from the 2009 depths, to “risk-off” time periods when defensive stocks ruled and yields collapsed (in 2011-‘12 and again in 2015-’16 when there were negative yields to maturity on up to $14 trillion of bonds). Then there was the pro-cyclical, synchronized global expansion in 2016-17 to what is now an out-of-phase period of dollar strength in 2018. In each case, investors have sought concentration in specific locales within the capital markets spectrum, at the same time avoiding key uncertainties. As the saying goes, markets hate uncertainty more than anything else, and for global investors, markets hate currency instability/uncertainties to boot. The dollar and the U.S. corporate earnings growth story predominate current investor focus, making it difficult for other stories to see the light of day, particularly with a layer of currency uncertainty thrown on top. The currency instability is more an Emerging Markets issue, as we see the Euro and Yen more likely to appreciate versus the dollar over a multi-year time horizon. But probably not this year.

It is possible that the narrative shifts to one not nearly as favorable to U.S. stocks – which discount a lot of optimism about the future or that the increasingly elevated extent of indexation of U.S. stocks has exaggerated all the good. The pressure on EM currencies and economies impacts the earning capacities of U.S. and international-domiciled multinationals, something that has not really been reflected in the performance dichotomy. It’s possible that the markets’ capacity to smile past Trump trade rhetoric may suddenly end, taking U.S. returns lower. International markets have been for sale all year, and at some point, you run out of sellers. Maybe the trade talk ends in a big bro-hug about a week after mid-term elections. All of the above is no more than loose speculation, but worth considering.

More realistically, abatement of the strong dollar squeeze on EM fundamentals and the related capital concentration into dollar assets may begin to ebb or reverse in 2019, should the Fed relent from its current rate-hike path and policy events evolve constructively abroad. Global investors are essentially playing to be well positioned into the coming year at this point.

What Turns This Around?

It’s axiomatic, but bear markets sow the seeds of the next bull markets because valuations compress irrationally. Values abound in the late phases of a bear market because the selling becomes reflexive and unthoughtful, leading to diamonds on the street, waiting to be picked up by investors with a modicum of patience and risk tolerance. In their later stages, the pessimism becomes abject and without clear drivers.

We see elements of this mindset in current (2H2018) discussions with clients. “Why bother with international, I should have put all my money in the U.S.”, has become an increasingly common discussion. That is more or less the tone you would expect when valuations have become abjectly cheap and devoid of expectations, with investors reflexively selling international positions to concentrate more capital in near-term winners. Today’s international markets are reminiscent of broader global market conditions in late 2011-2012, when valuations were compressed for just about everything – from tech to banks to industrials to durable goods, particularly after a sharp correction in stock prices in mid-2011. The rationales at the time tended to be vague macro negatives – the U.S. had lost its AAA rating from S&P, the Eurozone had a small rogue indebted state on its hands (Greece) and several large undercapitalized banks, the U.S. had an unresolved “fiscal cliff” of expiring tax brackets and incentives poised to jump absent legislative action, and business confidence was poor. None of these issues had very clear timeframes to resolution (or consequences for business valuation). If you could wind the clock back, it would have paid to be aggressive and buy the weakness and the daily negative headlines. But – much uncertainty as to when you would be rewarded.

Today’s catalogue of issues is a bit different from market anxieties of the 2011-12 time frame. Features of the Eurozone remain unresolved, such as Brexit talks and Italian budgets, and importantly the ECB still has yet to lift off from 0% interest rates. These factors ought to be resolved some time in 2019, if not sooner. Internal demand growth in Europe and Japan remain structurally slow, leaving their companies rather hostage to global growth rates, and EM financial challenges don’t help. We view the relative earnings growth superiority of U.S. companies as uniquely benefiting from the end-2017 tax cuts. Statistically, most companies’ earnings growth rates will have to come down in 2019. Nonetheless, financial flows have followed the growth. The U.S. technology sector has become enormous in terms of global capitalization, and ebullient tech sentiment further polarizes returns – as tech and internet valuations remain at the forefront of investor interests.

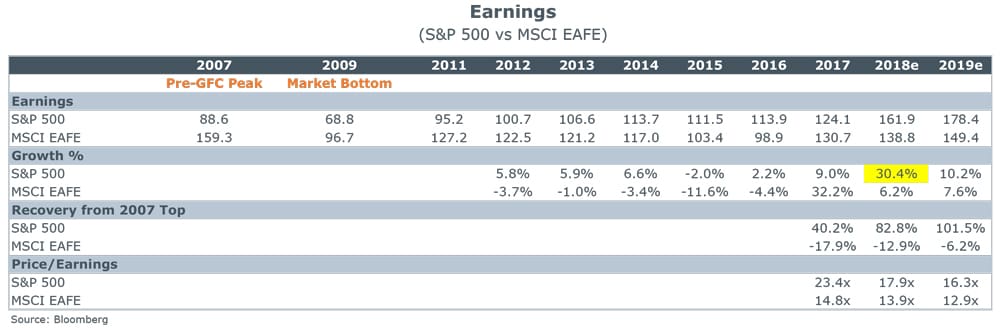

We believe the superior growth rate of U.S. corporate earnings will slow as the 2018 corporate cuts reach their anniversary. To wit, S&P 500 index earnings have grown from $100 in 2012 to $124 in 2017 (+24% or ~5% annually), and then accelerating to $162 in 2018e (per Bloomberg composite estimates). That is 30% growth this year. Lower tax rates form the bulk of this growth. The chances of reversion back to single-digit growth levels in 2019+ are quite plausible, and would be consistent with the 2011-2017 time period. Current consensus forecasts call for double-digit earnings growth into 2019 and beyond; this seems a stretch. Meanwhile, EAFE earnings have shown little consistency – declining from $122 in 2012 to a low of $98 in 2016, before rising back to the $138 level for 2018e. The EAFE earned about $120 in 2008, 2010, and 2011 as well. A stronger and more confident Europe (see below) could finally see some sustained earnings growth after a long slog bumping along at a rate first achieved in 2005.

We believe the superior growth rate of U.S. corporate earnings will slow as the 2018 corporate cuts reach their anniversary. To wit, S&P 500 index earnings have grown from $100 in 2012 to $124 in 2017 (+24% or ~5% annually), and then accelerating to $162 in 2018e (per Bloomberg composite estimates). That is 30% growth this year. Lower tax rates form the bulk of this growth. The chances of reversion back to single-digit growth levels in 2019+ are quite plausible, and would be consistent with the 2011-2017 time period. Current consensus forecasts call for double-digit earnings growth into 2019 and beyond; this seems a stretch. Meanwhile, EAFE earnings have shown little consistency – declining from $122 in 2012 to a low of $98 in 2016, before rising back to the $138 level for 2018e. The EAFE earned about $120 in 2008, 2010, and 2011 as well. A stronger and more confident Europe (see below) could finally see some sustained earnings growth after a long slog bumping along at a rate first achieved in 2005.

Looking Forward to Key 2019 Events

As the calendar turns into 2019, we see three critical “macro” events that may shape returns.

First, the U.S. Federal Reserve may pause rate hikes beyond the two (anticipated) increases slated for the rest of 2018, or flirt with a yield curve inversion by pressing rate increases. A pause would be cathartic for international money flows, while an inversion may at least challenge the global preference for dollars given the ominous financial signal it portends. The Fed is generally expected to raise interest rates to the 2.5% level by December. Given the behavior at the longer end of the curve, which has had a difficult time pushing above the 3.0% level, and based on Fed Chairman Powell’s recent Jackson Hole commentary, rate increases beyond the 2.5% may exceed “neutral” monetary policy. A move to 2.75% or 3.0% may very well invert the yield curve, particularly as the Fed balance sheet is also shrinking at this time.

Second, the ECB should begin the process of exiting from QE (slated for December 2018) and normalizing its interest rate regime in 2019. Success on this front would bolster the value of the currency as well as business confidence, along with ending (or at least mitigating) the capital concentration in dollar assets. On a trade-weighted basis, the Euro (about $1.15 currently) is generally viewed as an undervalued currency, with fair value closer to the $1.25-1.30 level. But given the interest rate differentials and a difficult-to-quash “what-if” question about bond yields and fiscal sustainability in weaker European countries, it probably continues to trade cheap. The Fed messaged “gradualism” and “data dependency” as it exited QE and ZIRP in 2015-17 to assuage market psychology with good effect. The ECB needs to message its new rules of the road as it stops buying sovereign bonds in massive quantities, probably messaging something similar along with “European Unity” of some form. We can only speculate what the exit plan may be – credit rating-based yield spread caps on weaker sovereigns versus the strongest countries seems like a good idea to us – but maybe they have a different plan. ECB President Mario Draghi will step down in late 2019 after a heroic stint, and legacy at this juncture matters. A better Euro as an alternative reserve currency to the dollar matters a great deal. Alongside European monetary normalization, we expect the terms of the U.K.’s Brexit “deal” to be solidified within the next 12 months, tidying up another key uncertainty for the markets.

Tighter U.S. monetary policy is a particularly difficult pill to swallow in Emerging Market economies. A stronger Euro would partially neutralize the strong dollar tourniquet that afflicts EM financial conditions. The dollar’s status as the dominant global reserve currency is amplified by current conditions, where it is the only major reserve currency with a positive short-term interest rate. As this rate has headed higher in 2018, funding stresses in weaker Emerging Markets have quickly erupted. Emerging markets have greatly benefited from low prevailing rates in reserve currencies. With most industrial products and commodities priced in dollars, a higher dollar on the back of higher U.S. rates creates double pressure on emerging economies in terms of import costs and financing. It is worth pointing out that U.S. interest rates were not “normal” until 2018, having remained below 1% up to the latter part of 2017. We would contend that Emerging Market financial stability will remain the largest question mark into 2019, as competitive-yield pressure from the U.S. and Europe could just make matters worse.

Last, China finds ways to grow – World demand depends little on Argentina or Turkey, but depends considerably on China. To date, China cut individual tax rates and has let its currency slip a little versus the dollar, while tightening up the exits by which dollars can leak out of the country. In 2009, China enacted aggressive fiscal and monetary stimulus plans to offset the GFC-induced global recession. These measures worked in aggregate, although much of the spending was widely acknowledged as having questionable merit. We currently anticipate a more targeted approach to stimulus, with higher value-added industries getting priority. China’s growth has slowed from the early 2010s to today, and we expect it will continue to slow. However, the country’s move up the value-added curve to greater prosperity is clear on a broad basis. In short, we would not underestimate these guys.

Conclusion

Beating a drum as to the merits of a true global asset allocation have become difficult, given the spectacular success of U.S. stocks in the decade of the 2010s. However, the virtues of asset allocation and diversification remain, despite the increased skepticism that is inevitable when returns have polarized in one direction or another. Contrary arguments suggest a “this time is different” conclusion, often a dangerous one to reach. The U.S. economy has more than fully recovered from the depths of the Great Recession, while other major Developed Market economies remain well below potential output. This set of factors has become all the more acute for market returns as the U.S. has normalized its monetary policy amidst full employment conditions. There are a number of reasons to believe that recoveries in international markets may gain steam in 2019-20 alongside international monetary conditions, while the ongoing success of U.S. equities may comparatively run on a bit less steam in the coming years.

Certain information contained in this communication constitute “forward-looking statements”, which are based on Cambiar’s beliefs, as well as certain assumptions concerning future events, using information currently available to Cambiar. Due to market risk and uncertainties, actual events, results, or performance may differ materially from that reflected or contemplated in such forward-looking statements. The information provided is not intended to be, and should not be construed as, investment, legal or tax advice. Nothing contained herein shall be construed as a recommendation or endorsement to buy or sell any security, investment or portfolio allocation.

Any characteristics included are for illustrative purposes and accordingly, no assumptions or comparisons should be made based upon these ratios. Statistics are based upon third-party sources that are deemed to be reliable, however, Cambiar does not guarantee its accuracy or completeness.

As with any investments, there are risks to be considered. Past performance is no indication of future results. All material is provided for informational purposes only and there is no guarantee that the opinions expressed herein will be valid beyond the date of this blog.