Choose Your Battles

Cambiar President Brian Barish examines the forces reshaping today’s market environment. As valuations remain elevated and uncertainty rises, the piece outlines why diversification, asset allocation, and valuation discipline matter more than ever.

Wars are Not the Time to Sell

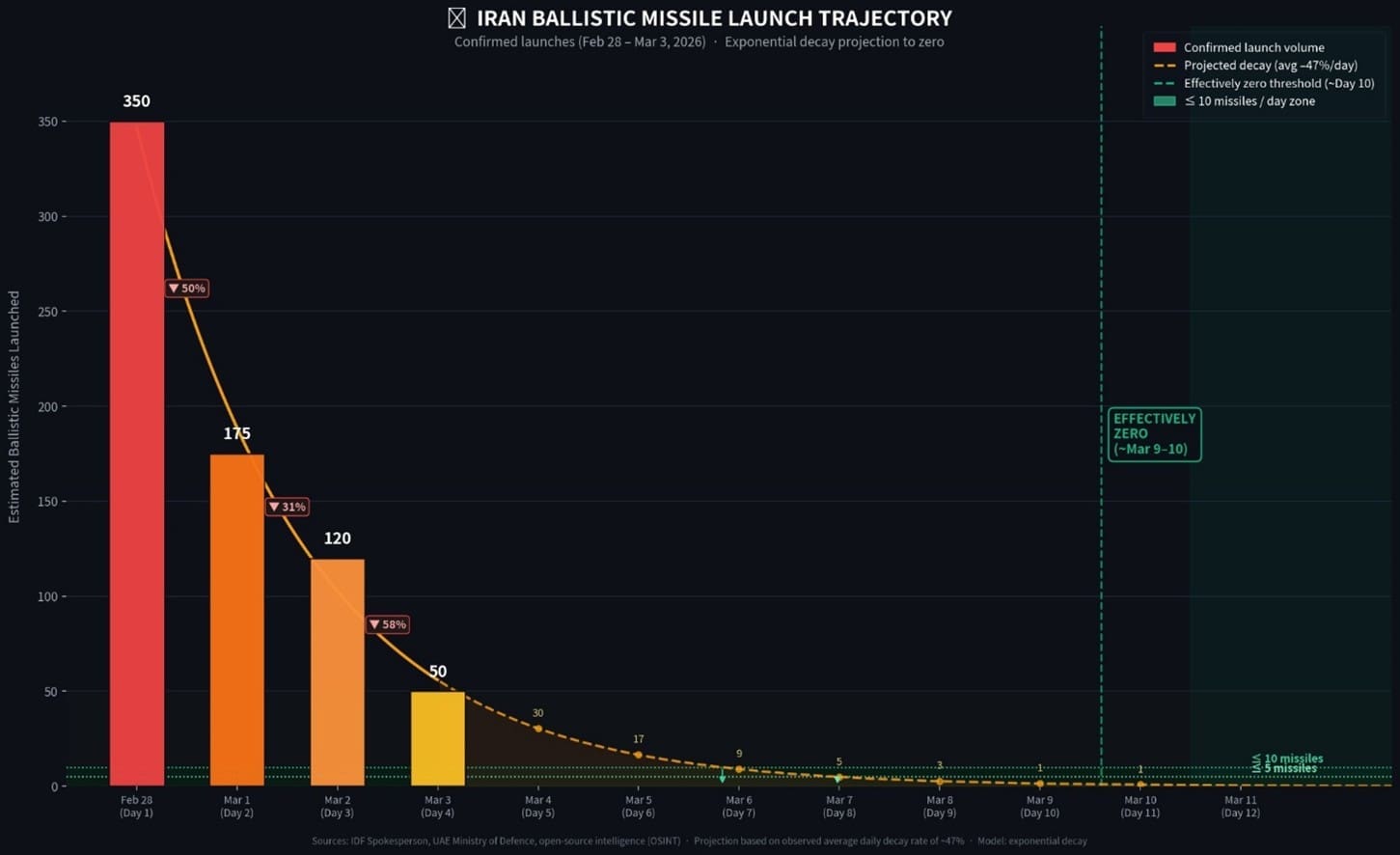

In the short run, we are leaning into names we already know and like well, as the market has begun to sell off a bit indiscriminately this week (owing to wartime uncertainties). In academic terms, risk premia are rising. Wars are just about the most uncertain form of human action – it’s very difficult to predict wins, losses, and longer-term effects. That said, the onset of hostilities is usually not a selling event (see any number of USA-led actions in the Mideast and South Asia). Toppling Iran is an audacious goal, but advanced weapons technology and precision munitions, coupled with air superiority, is practically impossible to sustain a fight against. It would appear the Iranian capacity to disrupt the Strait of Hormuz and lob missiles elsewhere is declining at a geometric rate, as depots are destroyed and any missile launches immediately light up on radar, leading to them being promptly taken out. It’s altogether surprising to see U.S. heavy bombers (70-year-old B-52s) already in use, suggesting there are no credible Iranian air defenses (a B-52 has the radar profile of a football stadium flying through the sky). These massive aircrafts carry a lot of munitions and can do significant damage.Getting past the war noise, we suspect that there is a good case for a degree of “multiple compression” in global equity valuations – a process that may run on for a few quarters once it gets started.

Assuming, for the moment, that Iran’s capacity to disrupt energy supplies and cause other forms of mischief is indeed defanged in the coming days, risk premia would quickly recede. Some larger issues would then seem likely to return to the forefront.

Multiple Compression?

Getting past the war noise, we suspect that there is a good case for a degree of “multiple compression” in global equity valuations – a process that may run on for a few quarters once it gets started. A less constructive outlook for valuations on the whole in 2026 coincides with some noted statistical tendencies, such as weaker returns in year 2 of a Presidency, and a propensity for market challenges in the months following a new Fed Chair appointment. These are admittedly small sample-set coincidences. Less coincidental is the starting point of 22x forward earnings multiple for the S&P 500 in January 2026. Valuations at this level have historically not been sustained for much more than a year (for non-recessionary earnings), with uglier outright declines more likely should the multiple expand to an even more expensive level.

Why would multiples compress? Besides the elevated starting point, there are three reasons to imagine equity markets may clear at a lower multiple one to two years from now.

- A narrative shift is underway in the (very large) AI-driven theme and related equities.

- Credit spreads are generationally low and probably due to rise.

- The next Fed Chair (Kevin Warsh) is a noted critic of the Fed’s large (and difficult to explain) balance sheet, a consequence of multiple rounds of QE in the 2009-2021 time frame. This topic probably won’t receive much ink for a few months, but we suspect another feature of the new world order will be less liquidity provided directly by the Federal Reserve through a large balance sheet and a return to (market-driven) interbank lending. We can see long term economic and political rationales for this policy shift, but do not see this change as particularly beneficial for asset valuations.

We won’t hazard a guess as to where stock multiples may settle. Lower than 22x. If they settled at 17-18x, or about where the “rule of 21” (i.e., 21 – 10 year yield = market P/E) would imply based on current interest rates, that is not so terrible in the larger scheme of things. But these kinds of processes are seldom especially smooth or predictable.

AI ROI

Yes, it’s big. Is it still awesome? It is observable that the AI narrative underpinning many of the largest index components has shifted in recent months to something less than “awesome”. Notably, intellectual property (IP)-driven businesses such as software and technology services have sharply de-rated in 2026. AI can code, scrape data, and replicate any number of bespoke functions that might have required customized software for business processes. Will the traditional software seat-license and maintenance model hold up peacefully as AI agents co-exist with humans as both users and the software’s foundations? It’s uncertain, and impacts both long term market size for these businesses as well as implying a business model transition risk. The starting point for software multiples at >32x earnings as recently as October left little room for questions about growth rates, TAM sizes, the business model, or terminal multiples. The space is lower now (perhaps due for a bounce), but these questions are unlikely to be answered in just a space of months. Nobody really knows! We would note that other very recent AI-infused narratives, such as transaction forum-shopping and displacing established hard-currency payment rails with stablecoins and crypto seem utterly far-fetched. Net, for any number of businesses with clear business model risk, we anticipate lower multiples will persist.

If there is truly going to be multiple compression on the horizon affecting the broader market, cloud computing and the related $teracap providers of it via data centers have to factor into the equation. Amazon, Microsoft, Google, and Oracle are your leading cloud services providers and have been outstanding stocks over the last 10+ years, condensing complexity and scale and IT room costs for any number of customers. As cloud infrastructure is infused with AI capabilities, does this increase capital intensity to uncomfortable levels? For 2026, that’s a yes. Over a longer arc, this still seems like a naturally oligopolistic space with major scaling benefits; that said, we are watching the spending carefully. Have these companies suddenly become chronically capital intensive overnight? If FCF is well less than 100% of earnings (it may be closer to 0% in 2026), this argues for decidedly lower multiples than have been sustained for the past 10+ years.

There are plenty of other equity managers and technology funds that are more assiduously focused on AI as it rapidly evolves and deployed. Our thought process is simple – can the ROI possibly be attractive at this scale of capital investment? With AI capex poised to increase another 20-50% in 2026 versus extraordinary levels in 2025, the math is daunting.

Credit Cycles are Still a Thing

It’s been 17 years since the last credit down-cycle ended. You might remember – it was called the Global Financial Crisis, or the GFC for short. Not too many economic events ever earn a universally known acronym. Post-GFC banking sector regulations were highly effective in de-risking banks from ever taking on the leverage that led to the GFC and the dubious credit structures that obfuscated specific credit risks. Between these enhanced safeguards and the sheer severity of the GFC, it was reasonable to expect the next legitimate credit cycle would be a long ways off. However, signs are mounting that there may be one inbound.

Into the lending gaps proscribed by regulations, private credit has barreled in, with a different layer of obfuscation, benefiting from limited disclosure. It’s impossible to say precisely what’s going on in private credit given this basic limitation. However, usually the roots of a credit downcycle come from overly rapid growth, leading to poor underwriting discipline and some degree of fantasy financials. And leverage then creeps in on top, green-lit by low spreads and other similar factors that would normally act as speed bumps. Banks and other credit originators should not grow their lending books at significant multiples of GDP growth, unless it happens counter-cyclically. Doing so implies overly rapid risk-taking and probably some willingness to take on risks that others would refuse. Investment grade credit from financially transparent borrowers has been excellent for multiple years, but has likewise led to obvious complacency. At the end of September 2025, the BBB corporate spread stood at a generational low of 89 basis points. A move up to more typical levels of 120-140 bps would mean little in the larger scheme of things, but should also not be expected to flatter stock market multiples. Will banks successfully steer clear of these risks given their tightly-regulated status? Time will tell – the scope of the private credit boom has been pretty broad. We are not in a hurry to add to bank exposure in our portfolios, and have been net sellers in the last few months. Valuations are not terribly demanding but are not very attractive either.

Calm as calm can be right now. How sustainable is this?

Regime Change at the Fed

Outside of a handful of Fed watchers who squawk frequently, the topic of a “whole new playbook” for the Fed’s conduct of monetary policy gets scant attention. This is coming, we suspect. It could be a nothing-burger apart from a couple of widely expected rate cuts upcoming in 2026. Or it could be quite material.

The severity of the GFC and its wide impact on all lending institutions meant that a critical artery of the circulation of money in the broader economy, the Interbank lending market, died very suddenly in September 2008. It stayed dead, with no credible alternatives emerging for the balance of 2008. In early 2009, under the leadership of Fed Chair Ben Bernanke, the Fed began the first of what would be several rounds of “Quantitative Easing”, or QE. Round one brought the balance sheet up above 12% of GDP or nearly double its prior size. This served to create reserves in the system and becomes a surrogate interbank lending market to some degree. Subsequent rounds had different justifications, such as offsetting the potential impact of higher bank capital requirements from various rounds of the Basel standards, to urging higher inflation expectations. The unfortunate over-reaction to the Covid-lockdowns of 2020 (the Fed seemed to conclude this would be a deflationary shock) brought the Fed heavily into new asset classes normally reserved for the private sector, such as mortgage-backed bonds, and led to them buying the bulk of the Federal Government’s bond issuance in 2020-22.

Explain the game plan here?

Much has been made about the difference between QE and outright money printing. QE entails augmenting bank reserves and not the currency in circulation – not a bad idea when bank capital and reserves are decimated. The rationale for QE jumped the reasonable test by underwriting wild excesses in government spending and likewise buying nearly 100% of net mortgage debt issuance in 2020-21 was very far afield from the more noble intentions of QE under Bernanke. Mission creep and then some.

Whether it was the early iteration of QE or the more recent vintage, one thing is reasonably clear: QE raises asset prices! Money creation starts in the financial system and does not necessarily leak into the broader economy of tradable goods. But within the financial system, financial assets benefit, from stocks to bonds to homes and other risk-assets. Multiple rounds of QE have coincided with the stock market more than doubling as a % of GDP, and with average housing prices rising far more rapidly than average disposable income levels.

Generally speaking, the above financial trajectories have not been bad for the person with an investable financial portfolio. Far from it. But let’s be honest with ourselves – if home prices simply inflate away from the capacity of the average borrower, this means a nation of renters at more modest income levels. This cannot be a great plan. The relationship between the stock market and GDP is more complex this – certainly many of the $teracap hyperscaler datacenter and internet platforms have become as dominant (if not more) so beyond U.S. shores. Nonetheless, it stands to reason that further expansion of all these relationships versus historical averages can and may run into limits, whether that’s home prices, stock market PEs, credit spreads, and the aggregate value of stocks versus their host economy. An ever expanding Fed Balance sheet is in our opinion (and more than a few others) a significant contributor to this dynamic. A flat to shrinking balance sheet may do the opposite.

What to Do?

Three things:

- Diversification – spread out your bets.

- Remember asset allocation; this stuff works.

- Pay close heed to what you are actually paying (for stocks and other things).

Periods like this tend to reward investors who resist concentration risk. Over the past several years, markets have been heavily influenced by a relatively narrow set of narratives and leadership groups. That environment can create the illusion that diversification is unnecessary. History suggests otherwise. When leadership shifts, policy regimes evolve, or capital flows change direction, portfolios that are overly dependent on a single theme or sector tend to experience the sharpest adjustments. Spreading exposures across industries, geographies, and business models does not eliminate volatility, but it meaningfully reduces the risk that one macro development dictates the outcome of an entire portfolio. In uncertain environments, diversification is less about maximizing returns and more about ensuring durability.

There are parallels between the current period and the late 1999-early 2000 internet and telecoms bubble. The narrowness of the 1999 bubble market featured a derisive view of the not nearly as cool traditional industrial and consumer businesses, dubbed the “old economy” back in 1999. The old economy stocks proceeded to hammer the new economy stocks into the relative-performance dumpster in the ensuing 6 years – doing just fine thank you versus catastrophic losses over on the Nasdaq. The absolute valuation extremes of the narrow performance winners circa early 2026 are not as outrageous as was the case in 1999. However the degree to which it may be difficult to envision the precise business model and financials of some of the digital economy, AI-led, and IP-based economy winners in the next decade or so – this strikes us as a fairly substantial risk factor. It’s just very early.

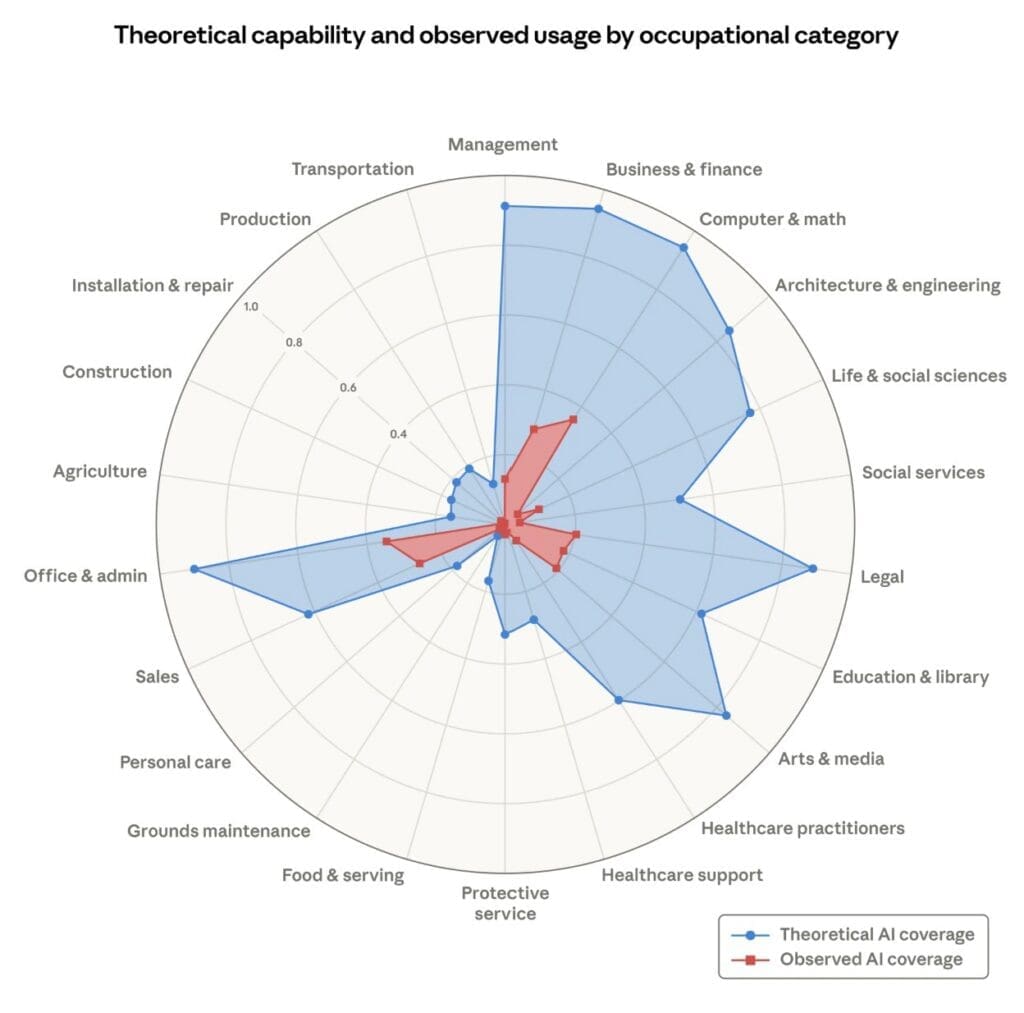

Source: Anthropic

Not unlike 1999-2000 we are finding value, and in some cases rather obvious value, in physical asset-businesses like railroads and rock quarries, over-sold consumer staples businesses, and main-line industrial businesses where there is little case for technological swap-outs or AI replication at fractions of the cost. The digital economy of the digital age does keep marching forward. We expect to invest in key platforms and enabling materials and chips, but some features may work a lot differently than current paradigms. So it goes.

Closely related to this is the simple but often overlooked power of asset allocation. Markets have a way of reminding investors that cycles still exist, even after extended periods of stability. Credit spreads move, liquidity conditions change, and valuation regimes eventually normalize. Maintaining a balanced mix of exposures across asset classes remains one of the most effective ways to manage these transitions. Asset allocation rarely receives much credit during strong equity markets, when concentrated positions can dominate results. But over full market cycles, it has consistently proven to be one of the most reliable drivers of long-term investment outcomes.

It’s not complicated, and it is certainly not a guarantee of any specific outcome. Markets may well continue higher through 2026 and beyond. But when starting valuations are elevated and multiple structural shifts are underway, discipline matters more than ever. Diversification, thoughtful asset allocation, and valuation awareness are not exciting concepts, but they have a long track record of working when market narratives begin to change. For now, we see enough moving pieces beyond the near-term military headlines to warrant a more careful approach. Investors would do well to choose their battles wisely.

Certain information contained in this communication constitutes “forward-looking statements”, which are based on Cambiar’s beliefs, as well as certain assumptions concerning future events, using information currently available to Cambiar. Due to market risk and uncertainties, actual events, results or performance may differ materially from that reflected or contemplated in such forward-looking statements. The information provided is not intended to be, and should not be construed as, investment, legal or tax advice. Nothing contained herein should be construed as a recommendation or endorsement to buy or sell any security, investment or portfolio allocation.

Any characteristics included are for illustrative purposes and accordingly, no assumptions or comparisons should be made based upon these ratios. Statistics/charts and other information presented may be based upon third-party sources that are deemed reliable; however, Cambiar does not guarantee its accuracy or completeness. As with any investments, there are risks to be considered. Past performance is no indication of future results. All material is provided for informational purposes only and there is no guarantee that any opinions expressed herein will be valid beyond the date of this communication.