All About the Business Cycle: Potential Tailwinds for European Banks

We examine why inflation and the war in Ukraine may only reinforce some of the strong business cycle trends found in the European banking sector.

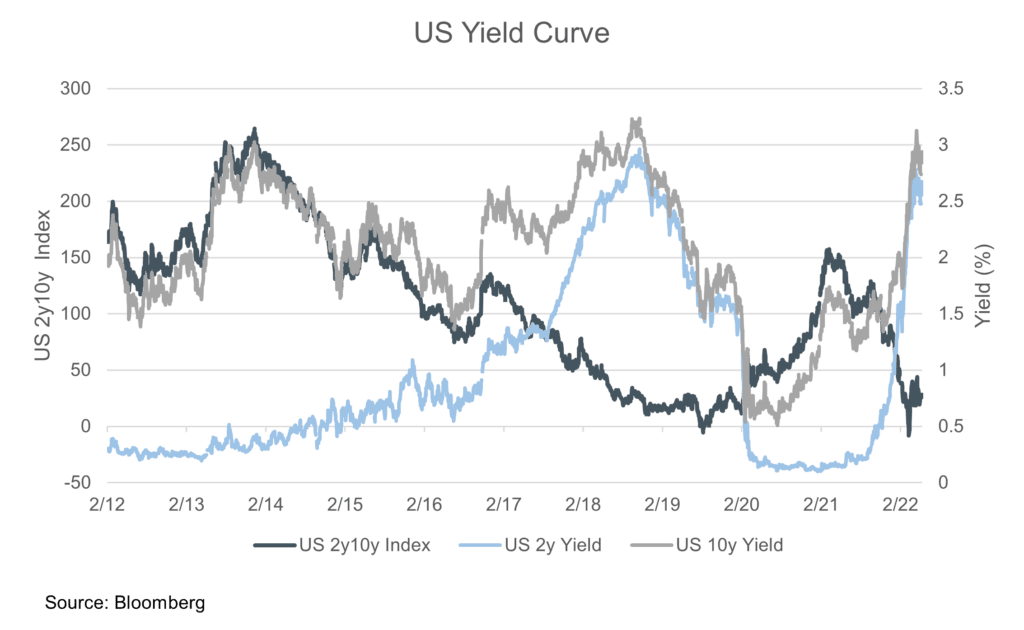

It should come as no surprise that the level and spread of interest rates matter for bank earnings. Yield curves also have a certain significance in markets – as discussed in the 1986 dissertation of Campbell Harvey, who found historical inversions of the 3-month/10-year spread to be a reliable barometer of impending recessions (provided the inversion in question persisted for a full quarter). It should therefore stand to reason that yield curve flattening is a poor environment for bank investors.

History, however, suggests that this is not always the case. European banks performed well in 2017, with the Eurozone Banks Index outperforming the EAFE Index by over 500bps – even as the yield curve flattened:

One reason for the outperformance during this period is that U.S. and Eurozone banks are far less reliant on wholesale funding today than in the run-up to the GFC. This means that bank stocks can perform even in a flattening environment as long as longer-end rates continue to drift up, which is what took place throughout 2017 and into early 2018.

Moreover, a flattening curve can coincide with the middle stage of the business cycle when the economy is strong enough to warrant the removal of central bank stimulus. This was exactly the type of bear flattening seen in 2017 – as the entire yield curve moved up, short-end rates moved more quickly than their counterparts to reflect the rapid repricing of policy expectations as the Federal Reserve stepped up its pace of hikes. The pattern repeated in the second half of last year, with bank stocks continuing their rally even as the 2-yr/10-yr flattened (though, it should be noted Mr. Harvey’s preferred 3-mo/10-yr indicator continued to steepen).

Rates matter, but they are not the whole story. Perhaps the most important message they deliver is in telling investors something about what stage of the business cycle an economy is in. After all, corporate earnings are what drive consequent stock performance. In 2017, bank stocks outperformed precisely because corporate margins were expanding, earnings gained momentum, and GDP growth consequently hit a fresh post-crisis high:

When it comes to investing in a highly cyclical sector like European banks, the lesson is simple but oft-neglected: one should always begin with an inquiry into the business cycle. Are investments being undertaken? Are consumer and corporate balance sheets healthy? Are profit margins expanding? And how does all of this translate into earnings and stock performance?

The four most expensive words in the English language are ‘This time it’s different.’

– Sir John Templeton

We are all aware of Sir John Templeton’s warning when it comes to saying something has changed in the investment climate; that said, the post-pandemic era is not the post-2008 era. We view calls for a return to secular stagnation to be misguided. One might even argue the investment climate that characterized the post-GFC secular stagnation world was the unusual paradigm, but that is beyond the scope of this commentary.

What we can say is that unlike the years after 2008 when demand was scarce, this cycle is defined by a resurgence in demand characterized by still-robust savings, tight labor markets, and households enjoying record real net worth.

One reason for the stronger demand environment is that governments reacted to the pandemic far more robustly by providing support to households and small businesses in a way that was not seen in the GFC period. Even the years of austerity in Europe have faded into memory as governments stimulated individually and through common issuance that would have been unthinkable a decade ago. Meanwhile, consumer and corporate balance sheets are in a much better place than they were in the lead-up to the financial crisis – meaning there is no imperative to deleverage in the same way.

Labor markets are tight as well, with unemployment in the U.S. nearly back to pre-pandemic lows, while the Eurozone continues to hit record low rates. For comparison purposes, the U.S. did not return to full employment post-GFC until the summer of 2015, a full six years after the end of the technical recession. The current rebound is happening much more quickly, which should make it evident that we are not back in the secular stagnation “normal”. This business cycle is different than the last one, which was very unusual for both its length but also its sluggishness.

The above comments are not the characteristics of a late-stage business cycle. While the war in Ukraine exacerbates inflation and creates potential harm to consumer balance sheets, consumers are still saving above the pre-pandemic trend, which means the buffer of savings continues to be reinforced. Moreover, major Euro-area governments from Germany to France have quickly stepped in to alleviate some of the rising burdens of fuel costs for households.

Nominal GDP in Europe also surpassed its pre-pandemic level as of the third quarter of last year, suggesting the economy is in a fresh phase of expansion driven by sustained demand. Most importantly, corporate profits have recovered soundly from the pandemic dip and are booming even more than in 2017 (the last period of Euro banks’ outperformance).

The strong trend in European corporate earnings is evident in the data. While the recent inflationary and geopolitical shocks are stagflationary in nature, the strength of corporate and household balance sheets coupled with an increasing, not decreasing, investment imperative in the face of geopolitical uncertainty should bode well for bank stocks. Strong corporate earnings coupled with a strong labor market are precisely the dynamics which drive the investment cycle so favorable to the performance of the banks.

The disconnect between the longer-run trend in corporate earnings and short-term market behavior suggests a favorable return opportunity for international equities. The disconnect is even more evident for bank stock valuations relative to their anticipated earnings. While there have been some downward revisions to estimates, the headwinds of inflation and war, we believe, are more likely to emphasize the need for further investment in supply chains and geopolitical security. The strength of the earnings boom should not be understated and emphasizes the speed with which earnings have returned to levels not seen since before the launch of QE in Europe (March 2015):

The early data on investment is encouraging as capital expenditure rises, driven both by the demand of reinvigorated consumers as well as the shortcomings uncovered in global supply chains after over a decade of post-GFC underinvestment. This is naturally in step with higher inflation, as the ECB mulls raising rates in the second half of the year – which should provide an additional tailwind to the beleaguered banking sector. The result is a forward return outlook for financials in general, and bank stocks more specifically, that is considerably more attractive than current valuations suggest.

The risk of Italian (or other Eurozone peripheral sovereign debt) spread widening in the context of rising yields bears mentioning. While structural issues in Italy remain unresolved, the European debt crisis was in large part the result of a perceived lack of common resolution facilities in the face of shocks. That fear was mitigated in 2012 by Draghi’s “whatever it takes” speech and the introduction of the outright monetary transaction (OMT) mechanism. While the program was never invoked, the evident institutional willingness to prevent a full-scale crisis was enough to rein in spreads at the time. Five other euro area countries also completed and exited bailout programs by 2018. The OMT program of targeted debt purchases, and its attendant conditionality for structural reform, remains an option for Italy together with the ECB’s stated willingness to “flexibly” adjust existing programs. While yields continue to drift up, the market should not underestimate the ECB’s crisis-fighting toolkit, nor the euro area’s commitment to the common project.

Here we return to the valuation of the pan-European Banking Index versus its history presented at the outset of this commentary. If we are to believe that we are no longer in this unusual era of secular stagnation and are instead in a world where consumer balance sheets are strong, corporate earnings are booming, the labor market is tight, and loan growth is accelerating, then the depressed valuation currently assigned to many EU banks begins to look even more compelling. Despite a markedly different macroeconomic setup, banks remain priced as though we are poised for a quick return to the world of secular stagnation. In our view, this does not make much sense in the longer term and is more a reflection of a growth scare disconnected from the fundamentals underpinning the sector.

2021 was a year of outperformance for financials within the EAFE Index. The sector was paced by the banks, as the ingredients of the early-stage business cycle combined to deliver strong nominal growth for the economy and consequent activity for the banks. 2022 had promised to continue these trends, with financials stocks outperforming the broader EAFE Index until the February 24th invasion of Ukraine. While growth prospects have deteriorated somewhat, we do think that the subsequent drop in sentiment towards the sector is overdone.

Comprising approximately 17% of the International Equity portfolio, Cambiar’s allocation to Financials attempts to strike a balance of offense and defense by return drivers. In risk-off environments, the portfolio takes advantage of the defense provided by names like Zurich Insurance Group or non-interest rate sensitive businesses like London Stock Exchange Group. At the same time, the portfolio has gently increased its exposure to cyclicality in line with the business cycle trends discussed above with the inclusion of names such as Barclays and ING Group and their outsized focus on the burgeoning recovery in consumer credit. In another positive data point for the banking sector, corporate lending also continues to hold momentum even as government assistance rolls off:

Certain information contained in this communication constitutes “forward-looking statements”, which are based on Cambiar’s beliefs, as well as certain assumptions concerning future events, using information currently available to Cambiar. Due to market risk and uncertainties, actual events, results or performance may differ materially from that reflected or contemplated in such forward-looking statements. The information provided is not intended to be, and should not be construed as, investment, legal or tax advice. Nothing contained herein should be construed as a recommendation or endorsement to buy or sell any security, investment or portfolio allocation.

Any characteristics included are for illustrative purposes and accordingly, no assumptions or comparisons should be made based upon these ratios. Statistics/charts and other information presented may be based upon third-party sources that are deemed reliable; however, Cambiar does not guarantee its accuracy or completeness. As with any investments, there are risks to be considered. Past performance is no indication of future results. All material is provided for informational purposes only and there is no guarantee that any opinions expressed herein will be valid beyond the date of this communication.

The specific securities identified and described do not represent all of the securities purchased or held in Cambiar accounts on the date of publication, and the reader should not assume that investments in the securities identified and discussed were or will be profitable. All information is provided for informational purposes only and should not be deemed as a recommendation to buy the securities mentioned.