Cheap Is Not Value

Learn why cheap does not equate to value.

The Cambiar International Equity strategy currently has a meaningful allocation to technology stocks. We are often asked about this portion of the portfolio, given that we are relative value investors and technology companies don’t appear to be “cheap” after a strong multi-year run. We’ve maintained that cheap does not equate to value, and that part of being a relative value investor is recognizing that value is a function of both price and quality – with the latter dictating the former. One important (yet not the only) metric Cambiar uses to define quality is a company’s Return on Invested Capital (ROIC), evaluated over a reasonably long timeframe. Why does ROIC matter? Let’s explore this question using a real company domiciled in Asia – we’ll label this Company A.

Company A was founded in the late 1980s as a semiconductor foundry that makes state-of-the-art semiconductors on behalf of its clients, which include a number of the leading global technology companies. As a foundry, Company A has a significant global market share for chip making and for the most advanced chips used in products such as smartphones, cloud data centers, artificial intelligence processors, autonomous driving, etc… The barriers to entry – in terms of capital, but more importantly technology – are immense. As such, we believe Company A will have a commanding lead over its competitors for the foreseeable future. Suffice it to say, the moats are very wide for this company. Like many leading edge companies, Company A invests a certain amount each year to produce more chips for clients and in order to grow its future sales and profits. Over the past five years, Company A has generated an incremental $0.24 for every $1.00 invested in the business, thus an ROIC of 24%. This is an excellent return, and exemplifies what we at Cambiar consider a great business. Put another way, Company A has 24% more capital every year with which it can then use to either reinvest back in the business to grow future earnings, distribute to shareholders through dividends or buybacks, or engage in accretive M&A. As investors, we place a higher multiple on higher ROIC companies because these companies can either compound earnings faster without having to borrow or issue equity, or have more distributable free cash flow after reinvesting in the business to give back to shareholders. In the case of Company A, it distributes about 30% of its excess free cash flow after capex to shareholders in the form of dividends, which at its current price amounts to nearly a 3% yield.

So how does the above example equate to what we believe is Relative Value? One way to illustrate this is by comparing Company A to two other real-life International companies and their stocks. For simplicity sake, we’ll label these two other companies Company B and Company C. Company B is a fast-growing challenger payment processor. As payments move from cash to electronic, and as consumers use different means to pay (Apple Pay, Alipay, Paypal, Square, etc…), this company’s processing technology has become more valuable (and more disruptive) to the established incumbent players that don’t have the capability to meet the needs of its merchants in the new digital era. Company B generates strong operating and free cash flow margins with Returns on Invested Capital also in the high 20s/low 30s. To be clear, this is an exciting company that we admire; however, this company currently trades on a 12-month forward P/E multiple of 126x.

So how does the above example equate to what we believe is Relative Value? One way to illustrate this is by comparing Company A to two other real-life International companies and their stocks. For simplicity sake, we’ll label these two other companies Company B and Company C. Company B is a fast-growing challenger payment processor. As payments move from cash to electronic, and as consumers use different means to pay (Apple Pay, Alipay, Paypal, Square, etc…), this company’s processing technology has become more valuable (and more disruptive) to the established incumbent players that don’t have the capability to meet the needs of its merchants in the new digital era. Company B generates strong operating and free cash flow margins with Returns on Invested Capital also in the high 20s/low 30s. To be clear, this is an exciting company that we admire; however, this company currently trades on a 12-month forward P/E multiple of 126x.

Company C is a legacy IT services provider with very little to no top-line growth, as parts of its business is being eroded away by the cloud, with new challenger companies competing away at the more leading-edge areas of IT services. The company generates a relatively low Return on Invested Capital of ~7%, but also trades at a low P/E multiple of just 10x.

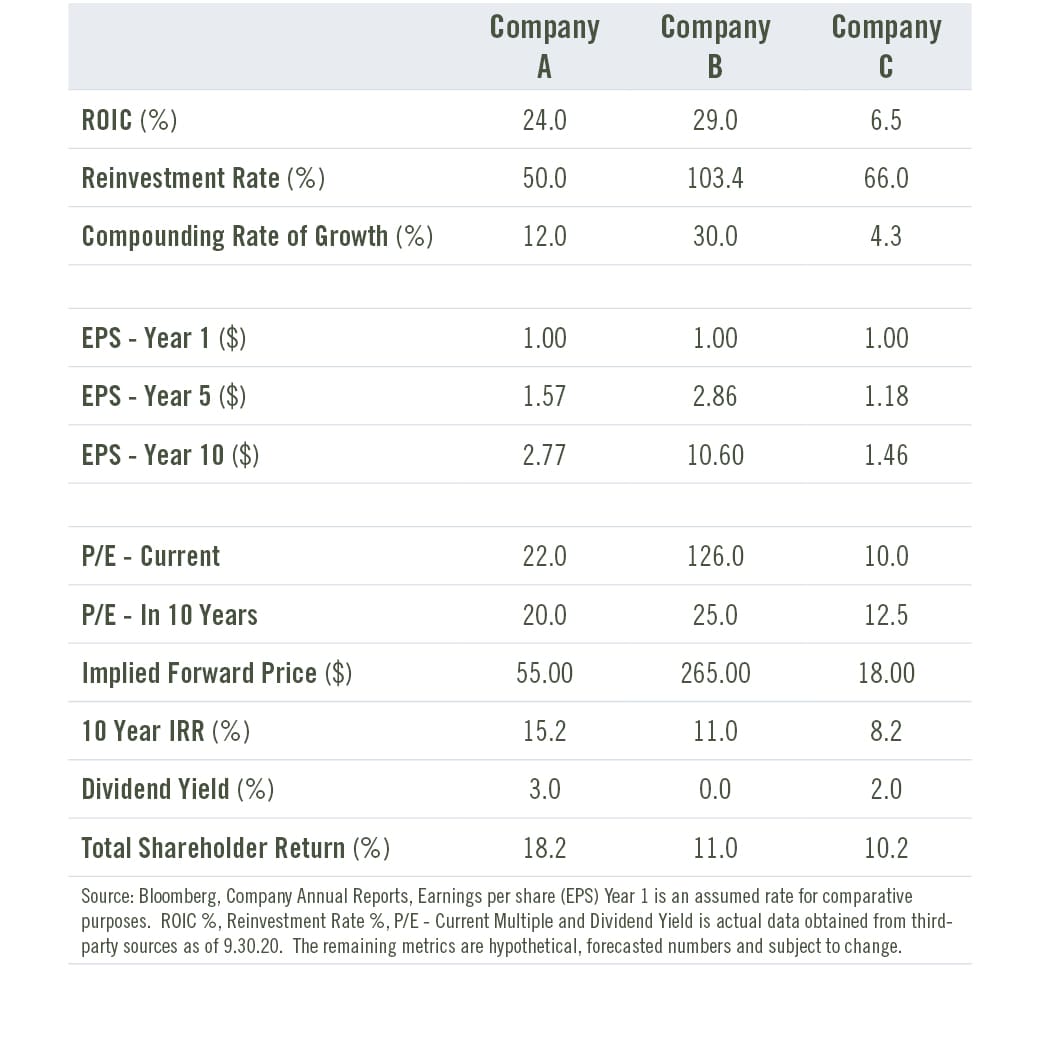

If we assume each of these companies generates $1.00 of earnings per share and we compound these earnings at their respective Returns on Invested Capital (after taking into account a certain level at which these companies have to reinvest back in the business to grow), we can get a sense of how fast these companies’ earnings can compound over a forward five or ten-year arc. By applying a reasonable multiple to those earnings into the future, we can then assess what kind of IRR (Internal Rate of Return on our investment) these stocks could potentially generate for us as investors if we purchased shares today. The table below shows all three companies and their forecasted earnings over five and ten years, using the same assumed current earnings per share.

In this illustration, Company A generates the far superior investment IRR, despite the fact that the company does not grow as fast as Company B and is not as cheap as Company C. This IRR also neglects the nearly 3% dividend yield that we would theoretically collect each year from Company A. We see that Company B, the fast-growing payment processor, should compound earnings at a much faster rate than Company A, but does not provide much margin of safety at its current multiple; in essence, the current stock price already embeds much of its future prospects. If Company B falls short of these lofty expectations, then the IRR to investors collapses quickly. Company C also generates an IRR lower than Company A despite its much cheaper valuation. That’s because we believe, despite its optically low valuation, its ROIC and sustainable rate of growth is too low to meaningfully compound earnings into the future. Furthermore, the risk here is that if earnings growth stalls – or even worse, were it to decline – given the lack of structural competitive advantages and excessive competition, the investment IRR turns negative fairly quickly as earnings power erodes over time. Therefore, the low multiple properly reflects what is deemed to be an inferior business model. To be fair, this is a very basic analysis and fails to take into account changes in end markets and product and service opportunities over time. As investors, we have to constantly monitor for changes in these opportunities or threats to these companies’ competitive positions in order to frequently reassess what we believe is appropriate fair value.

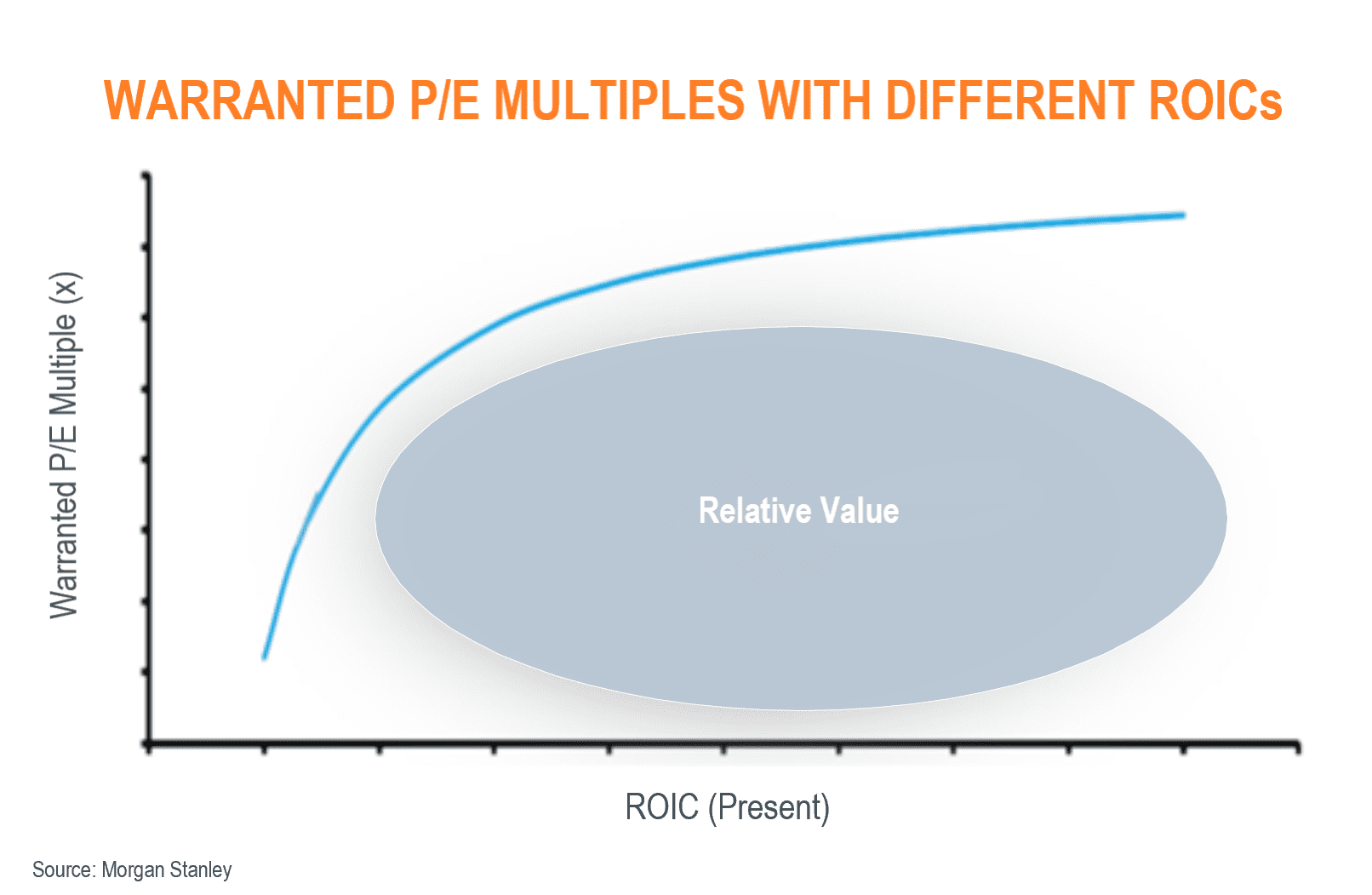

As relative value investors, Cambiar is striving to find a combination of reasonable valuations for above-average quality businesses. We don’t believe there are many that exist, hence our more concentrated approach to investing. The following chart, borrowed from Morgan Stanley, shows companies that can generate a high sustainable Return on Invested Capital tend to warrant a higher P/E multiple vs. those that generate poor Returns on Capital.

As relative value investors, Cambiar is striving to find a combination of reasonable valuations for above-average quality businesses. We don’t believe there are many that exist, hence our more concentrated approach to investing. The following chart, borrowed from Morgan Stanley, shows companies that can generate a high sustainable Return on Invested Capital tend to warrant a higher P/E multiple vs. those that generate poor Returns on Capital.

In other words, investors pay up for quality, and therefore higher quality companies get rewarded with a higher multiple by the market. What’s important for us as relative value investors is to be disciplined about what we pay so as to maximize the return on our investment and minimize the risk of a permanent loss of client capital. The “Land of Relative Value” sits below this efficient frontier where quality is not appropriately reflected in current valuations. That’s where we believe there are arbitrage opportunities to exploit market inefficiencies and deliver superior long term returns with a decent margin of safety.

At the moment, our technology companies across the Cambiar International Equity strategy generate ROICs that are well in excess of the average company within the overall benchmark itself. We’ve achieved this while paying a multiple that is below that of the average technology company in the benchmark. So we own businesses that have superior ROICs, while paying a below-average multiple. We believe technology companies, given their high barriers to entry – whether it be from specialized IP and/or network effects – offer investors the potential for high Returns on Capital in addition to secular tailwinds that allow for these businesses to compound for many years. Cambiar will continue to watch valuations, changes in the competitive landscape, and new opportunities that may arise that would alter our current view around future returns for clients, but for the time being, we remain comfortable with our overweight stance towards this space.

Certain information contained in this communication constitutes “forward-looking statements”, which are based on Cambiar’s beliefs, as well as certain assumptions concerning future events, using information currently available to Cambiar. Due to market risk and uncertainties, actual events, results or performance may differ materially from that reflected or contemplated in such forward-looking statements. The information provided is not intended to be, and should not be construed as, investment, legal or tax advice. Nothing contained herein should be construed as a recommendation or endorsement to buy or sell any security, investment or portfolio allocation.

Any characteristics included are for illustrative purposes and accordingly, no assumptions or comparisons should be made based upon these ratios. Statistics/charts and other information presented may be based upon third-party sources that are deemed reliable; however, Cambiar does not guarantee its accuracy or completeness. As with any investments, there are risks to be considered. Past performance is no indication of future results. All material is provided for informational purposes only and there is no guarantee that any opinions expressed herein will be valid beyond the date of this communication.

The specific securities identified and described do not represent all of the securities purchased or held in Cambiar accounts on the date of publication, and the reader should not assume that investments in the securities identified and discussed were or will be profitable. All information is provided for informational purposes only and should not be deemed as a recommendation to buy the securities mentioned.

Any illustrative models presented in this communication are based on a number of assumptions and are presented only for the limited purpose of providing a sample illustration of Cambiar’s investment process. Any sample illustration is inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond Cambiar’s control. Any sample illustration is not intended to represent the performance of any investment made in the past or to be made in the future by any portfolio managed or advised by Cambiar. Actual returns may have no correlation with the sample illustration presented herein, and the sample illustration is not necessarily indicative of any Cambiar investments. It should not be assumed that Cambiar’s investment recommendations in the future will accomplish its goals or will equal the illustration provided herein. A more detailed description of the assumptions utilized in any of the simulations, models, and/or scenario analyses is available upon request.